The US equity market is very different than before Election Day 2016, and that’s not just because we are at fresh all-time highs. There were plenty of new highs from 2013-2016, after all. What’s different is the lack of sector and asset class correlation now versus 2009 – 2016.

(Article by Tyler Durden from Zerohedge.com)

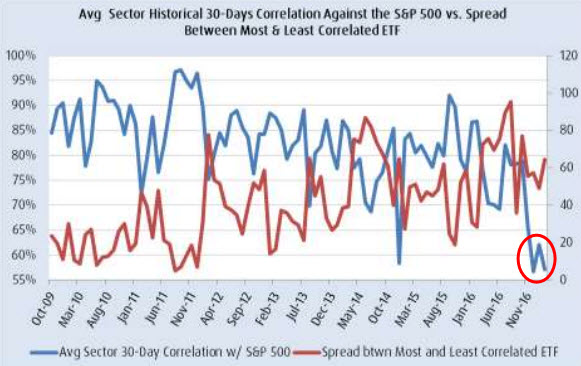

Simply put, they are finally back to normal. The drop in correlations among the 11 sectors of the S&P 500 has been profound, from 75-80% pre-Election to 57-62% afterwards. This month’s reading of 57% points to the lasting nature of the change; this is a not blip.

The ramifications of this shift are: 1) lower S&P volatility (because, math) 2) getting sector bets right is now even more critical to outperformance and 3) it applies not only to domestic US equities, but to global managers who must allocate to EAFE and Emerging Market assets (correlations are structurally lower there as well).

It has been 94 days since the US Presidential election and Donald Trump’s surprise win. In some ways it feels like yesterday, if only because it was not the expected outcome. And in other ways, it feels like it was years ago. Especially if you follow US equity markets, which have been remarkably quiescent. If a modern day Rip Van Winkle went to sleep on November 7th, woke up today, and looked at a chart of the S&P 500 he might think “Oh, Hillary Clinton won… And everything is status quo. I am a little surprised US stocks rallied so hard, but there’s no volatility. Yep – Hillary won.”

To see the effect of the Trump victory, you have to look at something other than price levels; you have to examine asset and sector price correlations. We have been doing this monthly since 2009, and the story has been largely the same. Correlations among the 10 (now 11) sectors of the S&P 500 have averaged 80-90%, and Emerging Markets and EAFE (Europe, Asia, Far East) equity markets have similarly tracked US equities. This was known as ‘Risk On, Risk Off” for much of the post 2009 period of market history. Everything goes up on the same days, and down on the same days.

Well, the world is very different now, and by a magnitude I would have thought impossible 95 days ago. We have attached some tables and charts to this note (click at the top for the PDF), but here is the highlight reel:

- Average sector correlations to the S&P 500 were 57.1% last month. On the eve of the US elections, they were 66% and for the prior year they had ranged from 70-80%. From 2009 – 2015, they were rarely below 80% and were +90% for 5 months straight in 2011. Since the election, sector correlations to the S&P 500 have been 56.8% (December), 61.2% (January) and that 57.1% reading we just mentioned. Keep in mind that 50% is a good estimate for a pre-Crisis long run average, and we are basically there now after almost a decade of unusually high correlations.

- The same observation holds for international equity markets. They have been tied at the hip to US stocks since the Financial Crisis as well, but now correlations for the EAFE country stocks to the S&P 500 are 61.4% and for Emerging Market equities it is 34.6%. The ramp down post-US election was a little slower. Correlations last month were 74.3% (EAFE) and 55.1% (Emerging Markets).

- The story in other asset classes is mixed. Precious metals (gold and silver) have been consistently in the low-correlation camp since 2009, and remain so today. High yield corporate bonds are seeing higher correlations to US stocks in the past month (now 72.9%, but 62.5% last month and 54.7% the month before that). High quality corporates and long dated Treasuries now sport (no surprise) a negative correlation to US stocks (-30.2% and -35.9%, respectively).

Since correlations were uniformly high before Election Day and now have reverted to much lower long term averages, we are going to chalk this up entirely to Donald Trump’s victory. Nothing else is sufficiently different so as to explain it. And as much as the recent spate of new highs is a welcomed development, we had new highs before the Election. The drop in correlations is really “New new”.

The big question is “OK, what does this mean?” Three thoughts to wrap up this note:

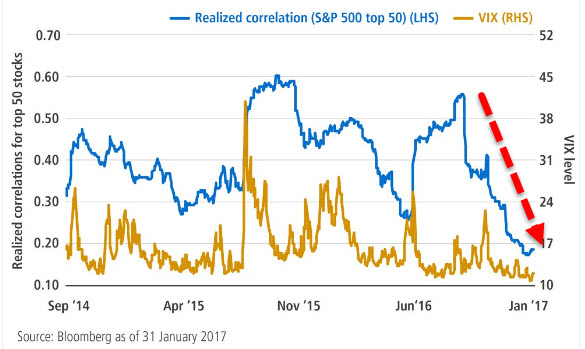

- Point #1: Lower correlations mean less price volatility in the S&P 500. That’s just math: the lower the correlation between assets in a portfolio, the lower the overall volatility. That’s one reason why the CBOE VIX Index has been so low (along with realized volatility). We’ll have to wait and see how much the sector correlations stay low when we get a systemic shock, but for now we can expect volatility to remain under pressure.

- Point #2: Getting sector and stock bets right just got a whole lot more serious. As correlations drift lower, different sectors will tend to show greater price and performance dispersion. Use Health Care as an example. Say you underweighted that group at the end of last year. Big mistake: it is up 4.1% year to date, and only overweights in Tech (+5.9% YTD) and/or Consumer Discretionary (+4.8% YTD) would have saved you so far. No other sector has better YTD performance than those three.

- Point #3: The same goes for international equity portfolios. Emerging markets are up 8.2% in dollar terms so far in 2017. EAFE is up 3.9% – more than the S&P 500’s 3.1% price return.

We will close with two reminders.

- Next week is St Valentine’s Day (Tuesday). Make sure whatever you might be getting your significant other arrives on Monday, not Tuesday. If you leave it up to UPS or FedEx or the local florist, your gift will arrive at 5pm. You don’t want to leave your special someone hanging, do you?

- The day after Valentine’s is the unofficial middle of the first quarter. The drop in correlations has put a lot of managers on the back foot. Just consider Financials – last quarter’s “It” sector has underperformed in Q1 (2.1% versus 3.1% for the S&P 500). Or Energy, last year’s big winner and with a lot of funds still overweight (down 3.3% YTD).

That’s the rough part about the sudden drop in correlation; being wrong just got a lot more expensive. Underperforming groups like Energy and Financials are on a short leash as we transit the mid-quarter point. They both worked today, but they have a lot of ground to cover. You might not see this turmoil on the market’s surface, but it is there. And it will most likely get even choppier.

Read more at: zerohedge.com

Submit a correction >>